NPS vs PPF comparison for 2025–26. Know returns, tax benefits, lock-in period, risk, and which option is better for retirement planning in India.

Introduction

Planning for retirement is one of the most important financial decisions you will make in life. In India, two of the most popular retirement investment options are NPS (National Pension System) and PPF (Public Provident Fund). Both have unique features, tax benefits, and risks. Many people often wonder, “NPS vs PPF: Which is better investment for retirement in India?”

In this article, we will compare NPS vs PPF in detail, including returns, tax benefits, flexibility, and risk. By the end, you will have a clear idea about which investment suits your retirement goals.

What is NPS?

NPS or National Pension System is a government-backed retirement scheme launched for long-term wealth creation. It allows individuals to invest a portion of their income in equity, corporate bonds, and government securities.

Key features of NPS:

- Managed by professional fund managers

- Investment in equity up to 75% (for young investors)

- Tax benefits under Section 80C and 80CCD(1B)

- Partial withdrawal allowed after 3 years for specific purposes

- Pension after retirement based on accumulated corpus

Benefits of NPS:

- Higher potential returns than PPF due to equity exposure

- Flexibility in investment allocation

- Low-cost investment with professional management

Limitations of NPS:

- Cannot withdraw full corpus before retirement

- Returns are market-linked, so risk is higher than PPF

- Mandatory annuity purchase at retirement for a portion of corpus

What is PPF?

PPF or Public Provident Fund is a long-term government savings scheme that is fully backed by the government. It is considered one of the safest investment options for retirement planning.

Official details ke liye NSI PPF Page par visit karein.”

Key features of PPF:

- Tenure: 15 years (extendable in blocks of 5 years)

- Interest rate is fixed and declared by the government quarterly

- Tax-free interest under Section 10

- Contributions eligible for tax deduction under Section 80C

- Loan facility available after 3 years

Benefits of PPF:

- Safe and secure as it is government-backed

- Tax-free interest and maturity amount

- Encourages disciplined long-term saving

Limitations of PPF:

- Fixed returns may not beat inflation in the long run

- Limited liquidity; partial withdrawals allowed only after 5 years

- Maximum contribution limit per year is ₹1.5 lakh

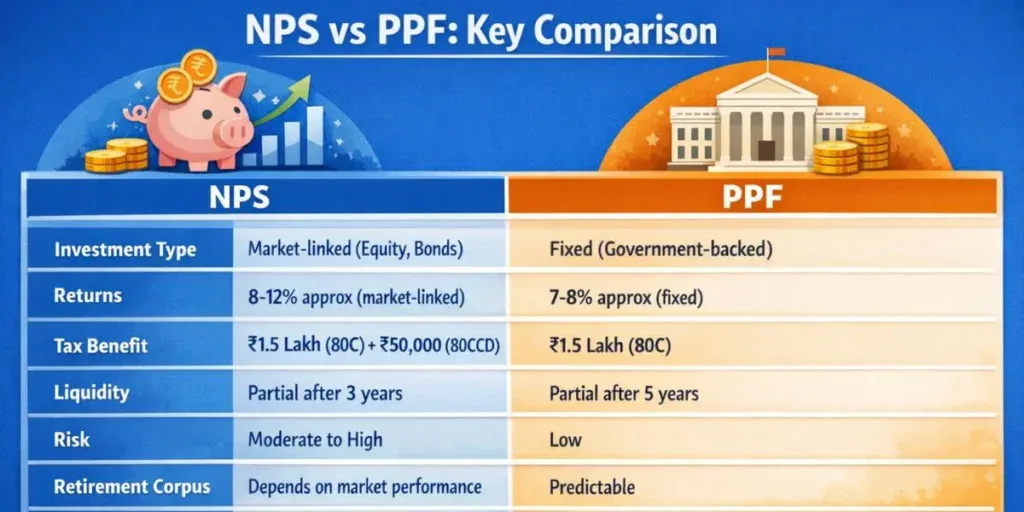

NPS vs PPF – Key Difference

| Feature | NPS (National Pension System) | PPF (Public Provident Fund) |

|---|---|---|

| Type | Market-linked retirement scheme | Government-backed savings scheme |

| Returns | 8–12% (market-based, not fixed) | ~7–8% (fixed, govt decided) |

| Risk Level | Moderate | Very Low |

| Lock-in Period | Till age 60 | 15 years |

| Tax Benefit | ₹1.5 lakh (80C) + ₹50,000 extra (80CCD(1B)) | ₹1.5 lakh under 80C |

| Tax on Maturity | 60% tax-free, 40% annuity taxable | Fully tax-free (EEE) |

| Liquidity | Limited withdrawals | Partial withdrawal after 7 years |

| Best For | Retirement corpus with growth | Safe long-term savings |

If your goal is regular monthly income after retirement, read Best Ways to Invest Retirement Money for Monthly Income in India 2026 for smart investment options.

NPS vs PPF: Which is better?

Choosing between NPS and PPF depends on your retirement goals, risk level, and return expectations. Both are popular long-term investment options in India, but they work differently.

Choose NPS If:

- You want higher returns with market exposure

- You are investing strictly for retirement

- You can take moderate risk

- You want an extra ₹50,000 tax benefit under Section 80CCD(1B)

- You have a long time (15–25+ years) before retirement

NPS invests in equity and debt, so returns are market-linked. Over the long term, it can generate higher returns compared to fixed-return options.

Choose PPF If:

- You want safe and guaranteed returns

- You prefer zero risk investment

- You want completely tax-free maturity (EEE benefit)

- You are looking for stable long-term savings

PPF is backed by the government and offers fixed interest, making it ideal for conservative investors.

If you are looking for a safe and fixed-return option, read Post Office FD Interest Rate 2026 – Latest Rates, Calculator & Maturity Returns for complete details.

NPS vs PPF: Which One Should You Choose?

When deciding between NPS vs PPF, consider your:

- Risk Tolerance: If you are young and willing to take moderate risk for higher returns, NPS may be suitable. PPF is better for risk-averse investors.

- Retirement Goals: For predictable corpus, PPF is safer. For higher potential growth, NPS is ideal.

- Tax Planning: NPS gives an additional ₹50,000 deduction under 80CCD(1B), which PPF does not offer.

Simple Rule:

- Choose PPF if you want safe, tax-free returns and disciplined saving.

- Choose NPS if you want higher potential returns with some market risk.

- You can also combine both for a balanced retirement portfolio.

NPS vs PPF: Returns Over Time

- PPF offers fixed returns of 7-8%, which is predictable.

- NPS returns vary based on market performance. Historically, NPS equity funds have delivered 9-12% returns.

- Inflation Adjustment: NPS may beat inflation over the long term due to equity exposure, while PPF may lag slightly if inflation rises.

For a low-risk and government-backed savings option, visit National Savings Certificate (NSC): Interest Rate, Benefits & Tax Saving Guide 2026

Pros and Cons Summary

NPS Pros: Higher returns, flexible allocation, tax benefits

NPS Cons: Market risk, partial liquidity, annuity requirement

PPF Pros: Safe, tax-free, predictable returns

PPF Cons: Lower returns, limited liquidity, fixed contribution limit

NPS vs PPF Interest Rate

PPF (Public Provident Fund)

- Interest Rate: ~7.1% per year (government fixed, quarterly review)

- Nature: Fixed & guaranteed

- Risk: Very low (Govt-backed)

NPS (National Pension System)

- Interest Rate: Fixed nahi hota

- Returns (average): ~8% – 12% per year

- Nature: Market-linked (Equity + Bonds)

- Risk: Medium (long term me better growth)

NPS vs PPF: Tax Benefits

NPS Tax Benefits:

- Investment under 80C: Up to ₹1.5 lakh

- Additional investment under 80CCD(1B): ₹50,000

- Partial withdrawal for specific purposes: Tax-exempt

- Pension (annuity) portion: Taxable

PPF Tax Benefits:

- Investment eligible under 80C up to ₹1.5 lakh

- Interest earned is fully tax-free

- Maturity amount is tax-free

Observation: NPS has higher total tax benefits due to the extra ₹50,000 deduction, but PPF is fully tax-free at maturity.

Conclusion

Both NPS and PPF are excellent retirement planning tools in India. Your choice depends on your risk appetite, retirement goals, and investment horizon.

- PPF is perfect for conservative investors looking for safe and tax-free returns.

- NPS is ideal for investors seeking higher potential returns and are comfortable with market risk.

- A combination of PPF + NPS can provide safety, tax benefits, and long-term growth.

In short, NPS vs PPF is not about which is better universally but which fits your retirement strategy.

Also read: FD vs PPF: Which Is Better Investment in 2026? (Returns, Tax & Safety)

Frequently Asked Questions (FAQ)

Q1. Can I invest in both NPS and PPF at the same time?

Yes, you can invest in both to balance safety and growth.

Q2. Which gives better returns for a 30-year horizon?

Historically, NPS equity funds may give higher returns over 30 years compared to PPF.

Q3. Is NPS risky?

Yes, NPS carries market risk, but long-term equity allocation can help mitigate it.

Q4. Can I withdraw NPS before retirement?

Partial withdrawal is allowed after 3 years for specific purposes. Full withdrawal is possible at retirement

Q5. Are PPF returns guaranteed?

Yes, PPF is backed by the government, and returns are fixed and predictable

Q6. Which is better for tax saving?

NPS gives additional deduction of ₹50,000 under 80CCD(1B), making it slightly better for tax saving than PPF.

Q7. Can I get pension from PPF?

No, PPF does not provide annuity. NPS requires buying an annuity for part of the corpus at retirement

very nice.