Post Office Monthly Income Scheme 2026 helps you earn safe monthly income. Check interest rate, eligibility, tax rules, and easy investment process.

The Post Office Monthly Income Scheme is one of the most trusted and safe investment options in India. It is backed by the Government of India and is perfect for people who want a regular monthly income with low risk. This scheme is especially useful for senior citizens, retired persons, and investors who prefer stable returns instead of market-linked risks.

In this article, you will learn everything about the Post Office Monthly Income Scheme, including interest rate, benefits, eligibility, investment process, tax rules, and more. The language is simple and easy to understand, suitable for an 8th-class level reader.

What is Post Office Monthly Income Scheme?

The Post Office Monthly Income Scheme (POMIS) is a small savings scheme offered by India Post. In this scheme, you invest a lump sum amount once, and then you receive fixed interest every month.

The interest is paid directly into your savings account, which helps you manage monthly expenses easily. Since it is a government-backed scheme, it is considered very safe.

Key Features

- Government-backed and low-risk investment

- Fixed monthly income

- Suitable for senior citizens and conservative investors

- Can be opened in single or joint account

- Easy account opening process at post office

Post Office Monthly Income Scheme Eligibility

To invest in the Post Office Monthly Income Scheme, you must meet the following conditions:

- You must be an Indian citizen

- Minimum age: 18 years

- A minor above 10 years can open an account through a guardian

- NRIs and HUFs are not eligible

Post Office Monthly Income Scheme Interest Rate

The Post Office Monthly Income Scheme interest rate is decided by the Government of India and may change from time to time. The interest is calculated on a yearly basis but paid every month, which helps investors earn a steady monthly income.

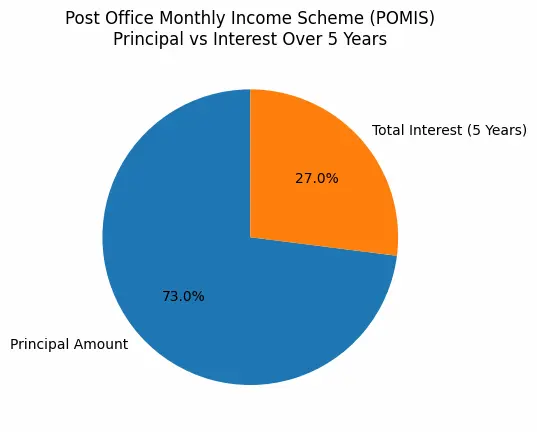

As shown in the pie chart, a large part of your investment remains safe as the principal amount, while the remaining portion shows the total interest earned over 5 years. This clearly explains how POMIS focuses more on safety with regular income rather than high risk returns.

Because the scheme is government-backed and offers fixed monthly payouts, it is a good option for people who want stable and predictable income, such as senior citizens and conservative investors.

Always check the latest interest rate at your nearest post office or on the official government website before investing.

Before investing, it is important to understand the POMIS interest rate & investment limits to plan your monthly income properly.

Post office monthly income scheme chart

| Period | Interest Rate (Annual) |

|---|---|

| 1st January 2026 – 31st March 2026 | 7.40% |

| 1st October 2025 – 31st December 2025 | 7.40% |

| 1st April 2025 – 30th June 2025 | 7.40% |

| 1st January 2025 – 31st March 2025 | 7.40% |

| 1st January 2024 – 31st March 2024 | 7.40% |

| 1st January 2023 – 31st March 2023 | 7.10% |

| 1st October 2022 – 31st December 2022 | 6.70% |

| 1st July 2022 – 30th September 2022 | 6.60% |

| Earlier Years (2017–2021) | Ranged around 6.6%–7.6 |

Planning long-term secure investments? Don’t miss Post Office Saving Schemes 2026: Interest Rates, Benefits & Best Plans in India for updated interest rates.

Post Office Monthly Income Scheme- Maximum Limit

- Single Account: Up to ₹9,00,000 can be invested.

- Joint Account: Up to ₹15,00,000 total investment.

- Minor Account: Separate limits may apply (guardian account).

- Important Rule: Even if you open multiple accounts, your total investment as an individual cannot exceed ₹9 lakh across all accounts (including your share in joint accounts).

Example:

- If you invest ₹9 lakh in your own POMIS account, you cannot invest more in another account under your name.

- In a joint account of ₹15 lakh, each person’s share is counted toward their ₹9 lakh limit.

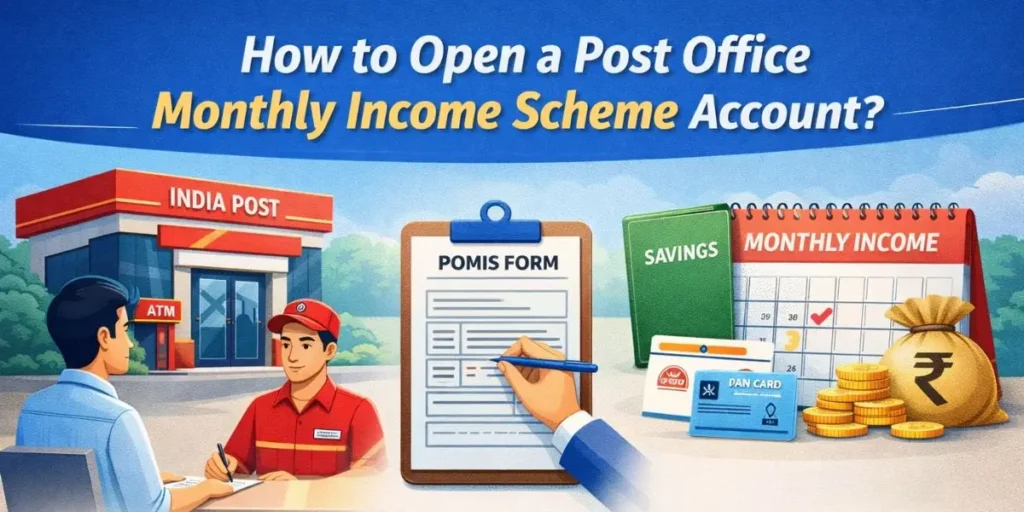

How to Open a Post Office Monthly Income Scheme Account?

Follow these simple steps to open a Post Office Monthly Income Scheme account:

“According to the MyScheme government portal, the Post Office Monthly Income Scheme offers safe monthly returns…”

- Visit your nearest post office

- Fill out the POMIS account opening form

- Submit KYC documents (Aadhaar, PAN, address proof)

- Deposit the investment amount

- Link your savings account for monthly interest

Looking for safe and stable returns? Read Post Office FD Interest Rate 2026 – Latest Rates, Calculator & Maturity Returns for complete details.

How Does it Work?

In Post Office Monthly Income Scheme, if you invest one-time money, and the post office pays you interest every month.

Example:

- Investment amount: ₹5,00,000

- Interest rate: 7.4% per year

- Yearly interest: ₹5,00,000 × 7.4% = ₹37,000

- Monthly income: ₹37,000 ÷ 12 ≈ ₹3,083

You will get about ₹3,083 every month in your savings account.

- Maturity period: 5 years

- After 5 years, you get your ₹5,00,000 back.

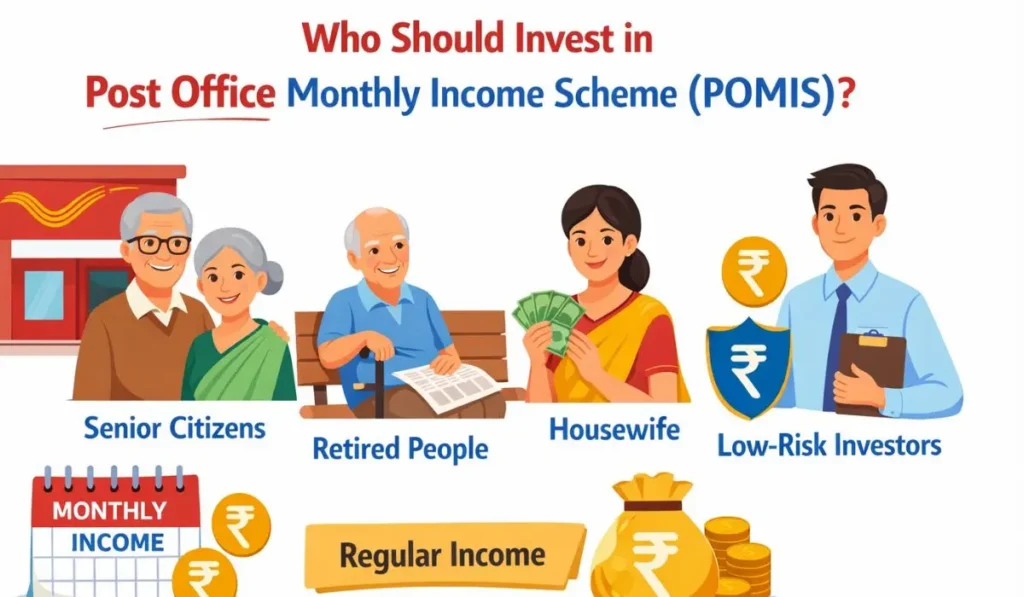

Who Should Invest in Post Office Monthly Income Scheme (POMIS)?

- Senior citizens looking for safe monthly income

- Retired people who want regular income

- Housewives needing steady earnings

- Low-risk investors who prefer safety over high returns

- Anyone needing fixed monthly income for expenses

This scheme is best for people who want stable and secure returns.

If your goal is regular monthly income after 60, explore Best Ways to Invest Retirement Money for Monthly Income in India 2026 for safe strategies.

Benefits of Post Office Monthly Income Scheme

1. Safe Investment

The biggest benefit of the Post Office Monthly Income Scheme is safety. Since it is backed by the government, your money is secure.

2. Regular Monthly Income

You receive interest every month, which helps in managing daily or monthly expenses.

3. Easy to Understand

The scheme is simple, with fixed returns and no market risk.

4. Joint Account Facility

You can open a joint account with up to three adults.

POMIS vs Bank FD vs NSC

| Feature | POMIS | Bank FD | NSC |

|---|---|---|---|

| Income Type | Monthly income | Monthly / Quarterly / At maturity | At maturity only |

| Safety | Very high (Govt-backed) | High (Bank-backed) | Very high (Govt-backed) |

| Interest Payout | Monthly | Flexible | No monthly income |

| Lock-in Period | 5 years | 1–10 years | 5 years |

| Tax Benefit | ❌ No 80C | ❌ No 80C (mostly) | ✅ 80C available |

| Best For | Regular monthly income | Flexible savings | Long-term tax saving |

Conclusion

The Post Office Monthly Income Scheme is a reliable and safe investment option for people who want steady monthly income without taking risks. With government backing, simple rules, and fixed returns, it is perfect for conservative investors and senior citizens.

Before investing, always check the latest interest rate and understand the tax rules. If safety and regular income are your priority, this scheme can be a smart choice.

Also read: National Savings Certificate (NSC): Interest Rate, Benefits & Tax Saving Guide 2026

Frequently Asked Question(FAQs)

Q1. What is Post Office Monthly Income Scheme?

The Post Office Monthly Income Scheme is a government-backed savings scheme that provides fixed monthly interest.

Q2. Is Post Office Monthly Income Scheme safe?

Yes, it is very safe because it is backed by the Government of India.

Q3. Can senior citizens invest in Post Office Monthly Income Scheme?

Q3. Can senior citizens invest in Post Office Monthly Income Scheme?

Q4. Is interest from Post Office Monthly Income Scheme taxable?

Yes, the interest earned is taxable under income tax laws.

Q5. What is the maturity period of Post Office Monthly Income Scheme?

The maturity period is 5 years.

Q6. Which Post Office Scheme is best for Monthly Income?

Post Office Monthly Income Scheme (POMIS) is the best scheme for monthly income.