Complete guide to Post Office Saving Schemes 2026. Check interest rates, tax benefits, eligibility, and compare the best post office investment plans for safe and guaranteed returns.

Introduction

Post Office Saving Schemes are one of the safest and most trusted investment options in India. These schemes are backed by the Government of India and are designed for people who want secure returns with low risk. From salaried employees to senior citizens, post office saving schemes are suitable for everyone who prefers stable and guaranteed income.

In this article, we will explain all major Post Office Saving Schemes in simple 8th-class level English. You will learn about interest rates, benefits, tax savings, eligibility, and which post office scheme is best for you.

What is Post Office Saving Scheme?

Post Office Saving Schemes are small savings plans offered through India Post. These schemes help people save money regularly and earn fixed returns. Since the government supports these schemes, the risk is very low.

These schemes are ideal for people who do not want to take market risks like mutual funds or shares. Post office saving schemes focus on safety, regular income, and long-term financial security.

Why Choose Post Office Saving Schemes?

Safe and Secure Investment

All post office saving schemes are government-backed. This means your money is safe, even during market ups and downs.

Fixed and Guaranteed Returns

Unlike market-linked investments, post office schemes offer fixed interest rates. You know your returns in advance.

Easy to Open and Manage

You can open a post office savings account easily with basic documents like Aadhaar and PAN card.

Tax Saving Benefits

Some post office saving schemes offer tax benefits under Section 80C of the Income Tax Act.

Post Office Saving Schemes List:

Post Office Saving Schemes Procedure & Eligibility

1- Post Office Savings Account

This is similar to a bank savings account. It is best for parking emergency funds.

Key Features:

- Safe place to keep money

- Easy deposits and withdrawals

- Interest is calculated yearly

2- Post Office Recurring Deposit (RD)

Recurring Deposit is best for people who want to save small amounts every month.

Key Features:

- Monthly investment

- 5-year lock-in period

- Suitable for salaried people

3- Post Office Time Deposit (TD)

Time Deposit works like a fixed deposit. It is available for 1, 2, 3, and 5 years.

Key Features:

- Fixed return

- 5-year TD gives tax benefits

- Ideal for short to medium-term goals

4- Post Office Monthly Income Scheme (POMIS)

This scheme is best for regular monthly income.

Key Features:

- Monthly interest payout

- 5-year maturity

- Good option for retirees

Complete Guide: Post Office Monthly Income Scheme 2026: Interest Rate, Benefits

5- Public Provident Fund (PPF)

PPF is one of the most popular post office saving schemes for long-term wealth creation.

Key Features:

- 15-year lock-in

- Tax-free returns

- Ideal for retirement planning

6- National Savings Certificate (NSC)

NSC is a fixed-income investment with tax benefits.

Key Features:

- Fixed maturity period

- Tax benefit under Section 80C

- Low-risk investment

Complete Guide: National Savings Certificate (NSC)2026: Interest Rate, Benefits

7- Senior Citizen Savings Scheme (SCSS)

This scheme is specially designed for senior citizens.

Key Features:

- Higher interest rate

- Quarterly interest payout

- Best for retirement income

Complete Guide: Senior Citizen Savings Scheme (SCSS) 2026: Interest Rates, Benefits.

8- Kisan Vikas Patra (KVP)

Kisan Vikas Patra is a safe post office saving scheme for people who want to double their money in the long term with guaranteed returns.

Key Features:

- Government-backed and low-risk investment

- Lump sum investment option

- Money grows steadily and doubles after a fixed period

- Suitable for long-term goals like education or wealth creation

9- Sukanya Samriddhi Yojana (SSY)

Sukanya Samriddhi Yojana is a special post office saving scheme designed for the financial future of girl children.Key Features:

- Account can be opened for a girl child below 10 years

- High interest rate compared to other small saving schemes

- Tax benefit under Section 80C

- Maturity amount is tax-free

- Ideal for education and marriage planning of daughter

Complete Guide: Sukanya Samriddhi Yojana Interest Rate 2026: Benefits, Rules & Calculator

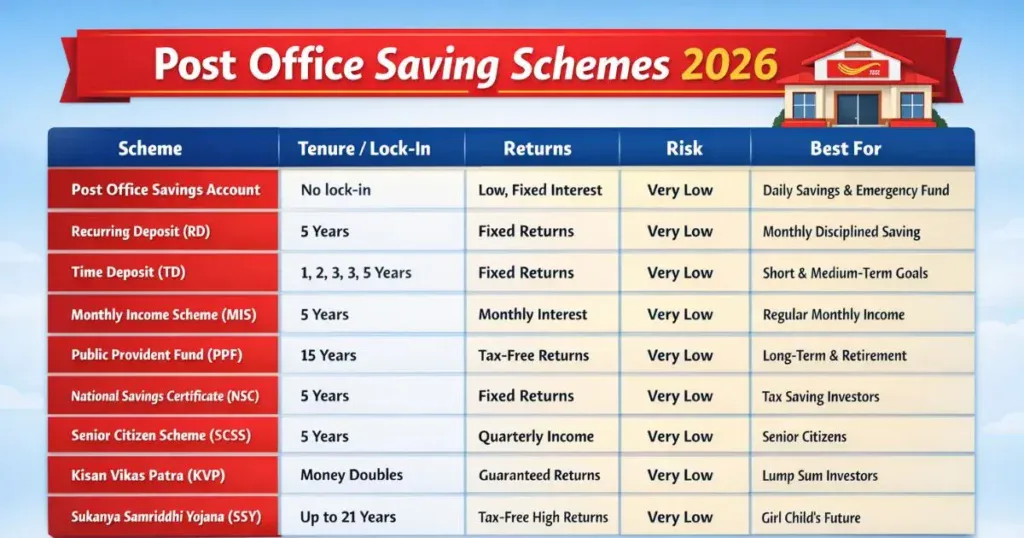

Post Office Saving Scheme Chart

| Scheme Name | Tenure / Lock-in | Returns Type | Risk Level | Best For |

|---|---|---|---|---|

| Post Office Savings Account | No lock-in | Low, fixed interest | Very Low | Daily savings & emergency fund |

| Recurring Deposit (RD) | 5 Years | Fixed returns | Very Low | Monthly disciplined saving |

| Time Deposit (TD) | 1, 2, 3, 5 Years | Fixed returns | Very Low | Short & medium-term goals |

| Monthly Income Scheme (MIS) | 5 Years | Monthly interest income | Very Low | Regular monthly income |

| Public Provident Fund (PPF) | 15 Years | Tax-free fixed returns | Very Low | Long-term & retirement planning |

| National Savings Certificate (NSC) | 5 Years | Fixed returns | Very Low | Tax saving investors |

| Senior Citizen Savings Scheme (SCSS) | 5 Years | Quarterly income | Very Low | Senior citizens |

| Kisan Vikas Patra (KVP) | Fixed tenure (money doubles over time) | Fixed returns | Very Low | Long-term wealth & lump sum investors |

| Sukanya Samriddhi Yojana (SSY) | 21 Years (partial withdrawal allowed) | Tax-free high returns | Very Low | Girl child education & marriage |

For safe and regular returns, read Post Office Monthly Income Scheme 2026: Interest Rate, Benefits & Returns before investing.

Post Office Saving Scheme Interest Rate

Interest rates of post office saving schemes are decided by the government and reviewed every quarter. Rates may change, but investments remain safe.

Different schemes offer different interest rates based on tenure and type of scheme.

Tax Benefits in Post Office Saving Schemes

Many post office saving schemes offer tax benefits.

- PPF, NSC, and 5-year Time Deposit qualify for tax deduction under Section 80C

- PPF maturity amount is tax-free

- Interest from some schemes may be taxable

Always check tax rules before investing.

Who Should Invest in Post Office Saving Schemes?

Risk-Averse Investors

People who do not want market risk should choose post office saving schemes.

Salaried Employees

Recurring deposits and PPF are good options for disciplined savings.

Senior Citizens

SCSS and MIS provide stable and regular income.

Long-Term Planners

PPF and NSC help in long-term wealth creation.

How to Open a Post Office Saving Scheme Account?

Follow these simple steps:

Post Office Saving Schemes – India Post Official Page

- Visit your nearest post office

- Fill the application form

- Submit KYC documents

- Deposit the initial amount

Advantages and Disadvantages

Advantages

- Government-backed safety

- Fixed returns

- Easy to understand

- Suitable for all age groups

Disadvantages

- Lower returns compared to equity

- Limited liquidity in some schemes

- Interest rates may not beat inflation

Post Office Saving Schemes vs Bank Fixed Deposits

Post office saving schemes are safer than bank FDs for long-term investors. While bank FDs depend on bank stability, post office schemes are directly backed by the government.

However, bank FDs may offer better flexibility in some cases.

Post Office Monthly Income Scheme (POMIS) vs Post Office Saving Scheme

| Basis | Post Office Monthly Income Scheme (MIS) | Post Office Saving Scheme (Savings Account) |

|---|---|---|

| Purpose | Regular monthly income ke liye | Safe parking of money & daily use |

| Risk | Very low (Government backed) | Very low (Government backed) |

| Returns | Fixed monthly interest payout | Low interest, yearly calculation |

| Investment Type | One-time lump sum investment | Flexible deposits & withdrawals |

| Lock-in Period | 5 years | No lock-in |

| Liquidity | Premature withdrawal with penalty | High liquidity (anytime withdraw) |

| Best For | Retired people, senior citizens | Emergency fund, daily savings |

| Tax Benefit | No 80C benefit | No major tax benefit |

| Interest Payment | Monthly | Yearly |

| Minimum Investment | Higher than savings account | Very low |

Conclusion

Post Office Saving Schemes are a perfect choice for people looking for safe, secure, and stable investments. These schemes help build saving habits and offer guaranteed returns with minimal risk. Whether you are planning for retirement, monthly income, or tax saving, post office saving schemes have an option for everyone.

Before investing, always understand your financial goals and choose the right post office saving scheme.

Also read: Post Office FD Interest Rate 2026 – Latest Rates, Calculator & Maturity Returns.

Frequently Asked Question(FAQs)

Q1. Which is the best saving scheme in post office?

There is no single “best” post office saving scheme for everyone. The best scheme depends on your goal, age, and income needs.

Q2. Are post office saving schemes tax-free?

Some schemes like PPF offer tax-free returns, while others have taxable interest.

Q3. Can I invest online in post office saving schemes?

Yes, some schemes can be managed online through India Post services.

Q4. Which post office saving scheme is best for monthly income?

Post Office Monthly Income Scheme (MIS) and SCSS are best for monthly or regular income.

Q5. Are post office saving schemes better than mutual funds?

Post office saving schemes are safer, but mutual funds may offer higher returns with risk.