Struggling with money? Learn the 50/30/20 rule step-by-step and take control of your finances, savings, and lifestyle without stress.

Introduction

Managing your money doesn’t have to be complicated. One of the easiest and most effective ways to take control of your finances is by using the 50/30/20 budget rule. But what is the 50/30/20 budget rule, and how can it help you save more, spend wisely, and achieve financial goals?

In this article, you’ll learn everything about this budgeting method — how it works, how to apply it in real life, and why it’s perfect for beginners who want to manage their personal finances smartly.

What is the 50/30/20 Budget Rule?

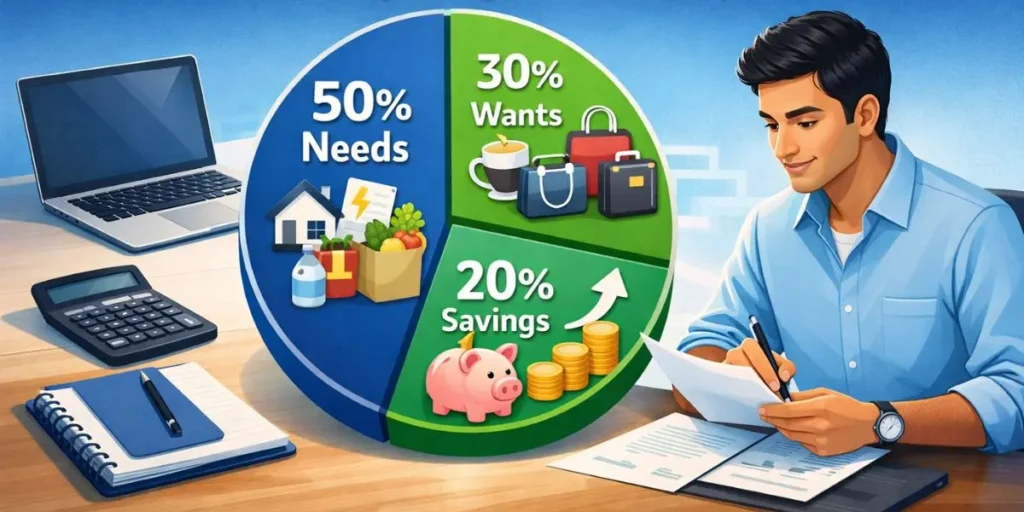

The 50/30/20 budget rule is a simple financial strategy that helps you manage your income effectively by dividing it into three categories:

- 50% for Needs – essential expenses you must pay

- 30% for Wants – lifestyle or fun-related expenses

- 20% for Savings and Investments – money for future goals and security

This rule was made popular by Senator Elizabeth Warren in her book All Your Worth: The Ultimate Lifetime Money Plan. It’s now one of the most widely used budgeting systems worldwide because it’s easy, practical, and flexible.

In short, the 50/30/20 budget rule helps you maintain a healthy balance between spending, saving, and enjoying your life without financial stress.

Why the 50/30/20 Budget Rule Works

The 50/30/20 budgeting method is effective because it gives you a clear framework for where your money should go. Many people earn decent incomes but struggle to save because they don’t track their spending. This rule ensures you’re always prioritizing essentials while still enjoying life and building wealth.

Here are a few key reasons why the 50/30/20 budget rule works:

1. Simplicity

You don’t need complex spreadsheets or apps. The rule is easy to remember and follow.

2. Flexibility

It can be adjusted for different income levels or lifestyles.

3. Balance

It encourages you to save without feeling deprived or guilty about spending on yourself.

4. Goal-Oriented

You always have at least 20% of your income directed toward future goals like savings, investments, and debt repayment.Breaking Down the 50/30/20 Rule

Let’s understand each part of the 50/30/20 budget rule in detail.

1. 50% – Needs

This category includes all your essential expenses — things you must pay to live and work comfortably.

Common examples of “needs” are:

- Rent or home loan (EMI)

- Groceries

- Utilities (electricity, water, internet)

- Transportation (fuel, public transport, maintenance)

- Insurance premiums

- Minimum loan repayments

Tip: If your needs exceed 50% of your income, it’s a sign that you might be overspending or living above your means. Try to reduce fixed expenses, like moving to a smaller apartment or renegotiating bills.

2. 30% – Wants

This portion covers expenses that make your life enjoyable but are not absolutely necessary. These are your lifestyle choices or “wants.”

Examples include:

- Dining out or takeaways

- Shopping or entertainment

- Vacations

- Subscriptions (Netflix, Amazon Prime, Spotify)

- Upgrading gadgets or clothes

The key is to enjoy these things without letting them take over your finances. Following the 50/30/20 budget rule keeps your spending under control while allowing room for fun.

3. 20% – Savings and Investments

This is the most powerful part of the 50/30/20 budget rule — your ticket to financial freedom. The 20% category covers:

- Emergency savings

- Retirement funds (PPF, NPS, EPF)

- Mutual funds or SIPs

- Stock investments

- Debt repayments beyond the minimum

- Future goals (buying a home, children’s education, etc.)

To make the most of your 20% savings, investing in SIP is a smart move—explore our expert picks in Top 10 Best Mutual Funds for SIP to Invest in 2026.

How to Apply the 50/30/20 Budget Rule

Let’s see how you can apply this rule practically to your monthly income.

Step 1: Calculate Your Monthly Income

Add up all your income sources — salary, side hustle, freelance work, or rental income. Use your net income (after tax) for accurate results.

Step 2: Divide Your Income Using the 50/30/20 Formula

Let’s assume you earn ₹60,000 per month.

- 50% for Needs → ₹30,000

- 30% for Wants → ₹18,000

- 20% for Savings/Investments → ₹12,000

Step 3: Track Your Spending

Use an app like Walnut, Money Manager, or Google Sheets to track every expense. Categorize them into Needs, Wants, and Savings.

Step 4: Adjust When Needed

If your rent or bills are too high, reduce discretionary spending. If you can save more than 20%, that’s even better!

Benefits of the 50/30/20 Budget Rule

Applying the 50/30/20 budget rule has several benefits that can transform your financial life.

1. Financial Clarity

You know exactly where your money goes every month.

2. Better Savings Habit

By consistently saving 20%, you build strong saving and investing habits.

3. Stress-Free Spending

You can enjoy your “wants” guilt-free because they’re already budgeted.

4. Improved Financial Health

With consistent savings and smart expense management, your financial health improves significantly over time.

5. Foundation for Financial Freedom

The rule ensures you spend less than you earn — the golden rule of wealth creation.

Common Mistakes to Avoid

While the 50/30/20 budget rule is simple, many people make mistakes that reduce its effectiveness.

- Not Tracking Expenses – You can’t fix what you don’t measure.

- Misclassifying Wants as Needs – Eating out or buying new gadgets often feels “necessary” but isn’t.

- Ignoring Debts – Always include debt repayment under the savings category.

- Being Too Rigid – Life changes, so adjust your budget when needed.

Adjusting the 50/30/20 Rule for Different Incomes

Not everyone’s financial situation is the same. You can customize the rule to suit your needs:

- If you earn less, shift to 60/20/20 (more for needs).

- If you earn more, try 40/30/30 to boost savings.

- For freelancers with variable income, use averages or create a flexible percentage each month.

The key is to maintain a balance — spend wisely, save regularly, and invest smartly.

Example of the 50/30/20 Budget Rule in Action

Let’s take an example of someone earning ₹1,00,000 per month.

| Category | Percentage | Amount | Example Expenses |

|---|---|---|---|

| Needs | 50% | ₹50,000 | Rent, bills, groceries, transport |

| Wants | 30% | ₹30,000 | Dining out, entertainment, shopping |

| Savings/Investments | 20% | ₹20,000 | SIPs, PPF, emergency fund |

By following this structure, you can easily track your financial flow and maintain discipline in your budget.

Tools to Help You Follow the Rule

Here are some apps and websites to simplify the 50/30/20 budget rule:

- Walnut – For automatic expense tracking

- ETMoney / Groww – For investments and SIPs

- Goodbudget – For envelope-style budgeting

- Google Sheets – For manual tracking and customization

Conclusion

The 50/30/20 budget rule is one of the simplest and most effective ways to manage your personal finances. By dividing your income into 50% needs, 30% wants, and 20% savings, you create a balance between enjoying life today and securing your future.

Whether you’re a student, working professional, or entrepreneur, this budgeting method helps you stay disciplined, reduce debt, and build long-term wealth.

Start small — track your expenses, follow the rule for 3 months, and notice how much easier it becomes to save money without sacrificing your lifestyle. Remember, financial freedom doesn’t come from earning more — it comes from managing better.

Also read: What is an Emergency Fund? Benefits, Importance, and How to Build It.

Frequently Asked Questions (FAQs)

Q1. What is the 50/30/20 budget rule in simple terms?

The 50/30/20 budget rule means you divide your income into three parts — 50% for needs (essentials like rent, food, bills), 30% for wants (entertainment, travel, etc.), and 20% for savings or investments.

Q2. Who created the 50/30/20 budget rule?

The rule was popularized by Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in their book All Your Worth: The Ultimate Lifetime Money Plan.

Q3. Why is the 50/30/20 budget rule important?

It helps you manage money easily, balance expenses, save regularly, and stay financially stable. It’s perfect for people who struggle with budgeting or overspending.

Q4. Can I change the percentages in the 50/30/20 budget rule?

Yes, you can. If your expenses are high, try 60/20/20 (more for needs). If you can save more, go for 40/30/30. The goal is flexibility while keeping savings a priority.

Q5. How can I start using the 50/30/20 budget rule?

- Calculate your monthly income after taxes.

- Divide it into 50%, 30%, and 20% portions.

- Track all spending using an app or Excel sheet.

- Review your budget monthly and make adjustments.

Q6. Does the 50/30/20 rule work for low-income earners?

Yes, but it may need adjustment. For low-income individuals, essential expenses might take up more than 50%. The key is to start saving something, even 5–10% monthly.

Q7. Is the 50/30/20 rule good for families?

Absolutely. Families can use this rule to plan household expenses, school fees, and savings goals while keeping finances transparent and organized.

Q8. Can I use the 50/30/20 rule if I have debts?

Yes. You can include debt repayments (beyond minimum payments) in your 20% savings category. The rule helps prioritize paying off debt and building financial security simultaneously.

Q9. What tools can help manage the 50/30/20 budget?

Apps like Walnut, ETMoney, Money Manager, and Goodbudget are great for tracking expenses and maintaining your budget automatically.

Pingback: “10 Easy Money-Saving Hacks for Beginners That Actually Work” - sujeetfinancehub.com

Pingback: What is an Emergency Fund? Benefits, Importance, and How to Build It - sujeetfinancehub.com